In the UK, the first online banking system was set up by the Bank of Scotland in 1983 – but the recipients included gas, electricity and telephone companies and other banks; and not their customers. Only in October 1994 were online banking services offered to members of the public, first by Standford Federal Credit Union.

Nowadays, there are hundreds of Online Banks – some acting as another resource for standard brick and mortal branched banks, others based purely online.

Banks now operating Online in the UK

Abbey National Building Society | Darlington Building Society | ||

Ahli United Bank | DirectLine | ||

Alliance & Leicester | Dudley Building Society | ||

Anglo IrishBank | Dunfermline Building Society | ||

Amber Homeloans | The Ecology Building Society | ||

Bank of Ireland | Earl Shilton Building Society | ||

Bank of England | Egg | ||

Bank of Scotland (HBOS) | First DirectBank | ||

Bank of Wales | Ipswich Building Society | ||

Barnsley Building Society | ING Direct | ||

Barclays Bank | Kensington Mortgages | ||

Bern Savings Bank | Kent Reliance | ||

Birmingham Midshires (HBOS) | Legal & General Bank | ||

Bradford & Bingley Building Society | Lloyds TSB Bank plc. | ||

Britannia Building Society | LombardDirect | ||

Bristol & West plc | The Leeds and Holbeck Building Society | ||

The Bath Building Society | National Westminster Bank (Natwest) | ||

The Beverley Building Society | National Counties Building Society | ||

The Buckinghamshire Building Society | Newbury Building Society | ||

The Cambridge Building Society | Newcastle Building Society | ||

The Cheshire Building Society | Northern Bank | ||

C Hoare &Co | Nationwide Building Society | ||

Cahoot | Nottingham Building Society | ||

CapitalOne bank | Standard Chartered Bank | ||

Catholic Building Society | Standard Life Bank | ||

Cheltenham & Gloucester | Sun Bank | ||

Chelsea Building Society | The Stroud and Swindon | ||

Chesham Building Society | The Swansea Building Society | ||

Chorley & District Building Society | Tesco | ||

Citibank | Tipton and Coseley | ||

CIS | TSB Bank | ||

Close Brothers | Ulster Bank | ||

Clydesdale Bank plc | Vernon Building Society | ||

Co-operative Bank | Virgin Direct | ||

Coutts | Woolwich plc | ||

Coventry Building Society | West Bromwich Building Society | ||

Cumberland Building Society | Yorkshire Bank | ||

As mentioned in ‘E-Commerce’, these are a few of the benefits, detriments and my uses of Online Banking

For the User

The benefits of Online Banking – for the user

- They can transfer money far quicker and at any time of the day

- No queuing – so it is convenient and less time consuming and tedious

- There is the convenience of not having to leave the home so it makes dealing with money that little bit less stressful

- Instant information from the bank – so no need to wait and waste any more time than necessary

- No need to fill in cards as all details are stored

- Charges are often lower than for ordinary accounts and accounts may offer higher interest rates

The detriments of Online Banking – for the user

- Computer illiterate people may find this difficult and complicated

- Online banking is open to fraud and scams and people can lose money (although, whether or not it is more open to fraud than normal banking is debatable)

- Money cannot be obtained from the computer – you still obviously have to go and withdraw from a bank

- In an attempt to keep personal details secure banks have users enter a pin or some other sort of pass code that allows them, and only them, access to their information – this can be annoying to the customer because although it is there for their privacy and protection, it is one more thing they need to remember

- When the site becomes updates or upgraded, you may have to re-enter your account information

For the Company Owner

The benefits of Online Banking – for the company owner

- Online banking allows the banks to reach out to more customers than previously possible through traditional banking branches

- Can reach out to a broader variety of customers – not just those within distance of their location branches

- Saves money as it is cheaper than opening a new branch in a new location – this allows them to offer their customers reduced transfer fees and other savings so they become more price competitive against other banks

- Also cheaper for banks as there is less paper and postage involved

The detriments of Online Banking – for the company owner

- Online banking requires lots of personal information and some customers will find it difficult to give this away over the internet with confidence

- Many people feel uncomfortable with new things and aren’t willing to work out through the learning curve when it comes to their money

- Even though the reduction in the use of paper is good for the environment, many customers prefer to have a paper trail for when they pay their bills

- No interaction with their customers so there is less trust and commitment from them – so they won’t feel as bad switching to another bank is there is no relationship

- Online banks cannot accept cheques or cash

My uses of Online Banking

As I do not have a bank account at all, I have never personally trialed online banking. But even if I did I am not sure whether or not I have enough trust in online banking just yet. I am well aware that there are some people with hacking skills and knowledge that the idea of having my personal and financial details online is a bit scary for me. A family friend was almost scammed once until the bank actually got involved and had to sort out the problem – so this hasn’t improved my confidence in Online Banking. I would much prefer taking the trip to my local bank if it means I have personal interaction with the person who is handling my account and my money.

Security

Online Banking basically has two different main methods of security – the PIN/TAN system, and signature based banking

- PIN/TAN – the PIN represents a password used for the login, and the TANs represent one-time only passwords. TANs can be dispersed in many ways such as; postal letters, security tokens or by SMS.

- Signature based – all transactions are authorized and encrypted digitally.

Internet only Banks

A few examples of Online-Only Banks include ‘egg’, ‘First Direct’, and ‘Smile’. Internet-based banking has formulated out of the success brought about by Banks offering online services to customers. By offering better interest rates and better features, online banks distinguish themselves from their forerunners.

The benefits of Online Only Banks

- Convenience – because it’s all online

- You wouldn’t have to change banks if you move house

- Free services e.g. free checking

- May give more information than a traditional bank site, as it is technologically adept

- Savings from being based only online and not having to support branches, are passed on to customer

The detriments of Online Only Banks

- You are stuck with any ATM fees the company gives you as they obviously don’t have any physical branches near your home

- You have to mail in your deposits

- If a payment is due on a specific day, you have to put in a check request days in advance

Ways in which Online Banks and Online Only Banks Entice Customers

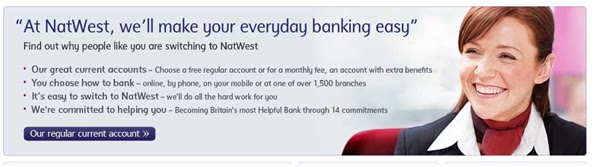

Online Bank Example - NatWest

- At the top of the home page there is a company quote, giving positive feedback on the bank

- At the bottom of the home page there are various links to customer services that hope to make their experience on the site as comfortable as possible

- The layout of the site attempts to be simplistic but formal and friendly in order to appeal to as many customers as possible as helpful but professional.

- There is a search panel at the top to help customers navigate and find exactly what they are looking for

Online Only Bank Example - Smile

- The animated advert at the top centre shows the latest offers - this captures customers' attention

- Animated pictures showing more offers also draws customers attention to them

- Smile's layout is a bit less formal than that of NatWest, but is consistent and the site is as user friendly as possible with tools such as site map and important information at the bottom

Both sites seem just as eager to promote it's latest deals on offer, and seem to share the aim of wanting a simplistic layout that will appeal to customers who want an easy, preferably inexpensive, banking experience.

No comments:

Post a Comment